Islamic Global Listed Infrastructure Equities

Executive Summary

Infrastructure equities can be play the role of “defensive engine” inside a diversified portfolio: they provide exposure to essential services—keeping the lights on, clean water flowing, goods and people moving, and data connected—often supported by resilient demand, predictable cashflows and above-average income potential.

Shariah compliance doesn’t remove the infrastructure opportunity; it refines it. Applying Shariah screens reduces the eligible universe, but it also reshapes sector and regional exposures—creating a distinct subset of infrastructure equities with different macro sensitivities. For Islamic multi-asset portfolios—where diversification can be constrained and equity benchmarks can be technology-heavy—Islamic listed infrastructure equities can help fill a meaningful gap.

Benefits of investing in infrastructure equities

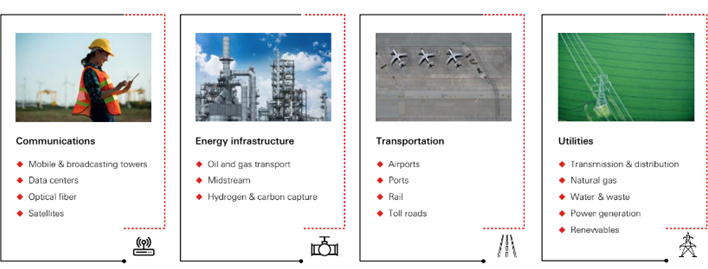

Infrastructure is best understood as the physical assets and networks that deliver essential services that economies and societies rely on every day. These assets typically operate across four broad sectors: communication, energy, transportation and utilities.

Click the image to enlarge

Many infrastructure assets share a set of potentially attractive features for investors:

- Essential-service demand: usage is often less discretionary, which can support more resilient revenues across economic cycles.

- High barriers to entry: large upfront capital requirements, long development timelines, and regulatory/permitting complexity can limit competition.

- Long asset lives: assets are built to operate over decades, supporting long-term planning and reinvestment.

- Predictable cashflows: revenues are often shaped by regulation (tariff frameworks and allowed returns) and/or long-term contracts (including take-or-pay style arrangements in certain segments), which can improve cashflow visibility.

- Potential inflation linkage: where tariffs or contracts include indexation or periodic resets, cashflows may have some ability to keep pace with inflation.

Listed infrastructure equities refer to publicly traded companies that own and/or operate infrastructure assets worldwide. They have grown meaningfully over the past decade, as investors increase the allocation to the asset class:

- Liquid alternative to direct infrastructure: investors can access infrastructure exposure immediately and adjust allocations efficiently

- Income potential: infrastructure assets are typically long-duration in nature, generating potentially high distribution levels

- Defensive building block within equities: resilient cashflows can underpin a more defensive equity profile

Shariah compliance: an evolution, not just a constraint

Shariah-compliant investing is an approach that seeks to align investment activity with Islamic principles. In listed equities, this is typically implemented through a transparent screening framework:

- Business activity screens: Companies are excluded if they derive material revenue from prohibited activities such as alcohol, conventional financial services, gambling, pork-related products, and military/weapons of mass destruction.

- Financial ratio screens: Companies are assessed against measures such as debt and cash/interest-bearing securities relative to market value or assets.

For infrastructure investors, the financial ratio screen is often the more consequential, because many conventional infrastructure business models use higher level of leverage.

Shariah investing principles reshapes the infrastructure opportunity set

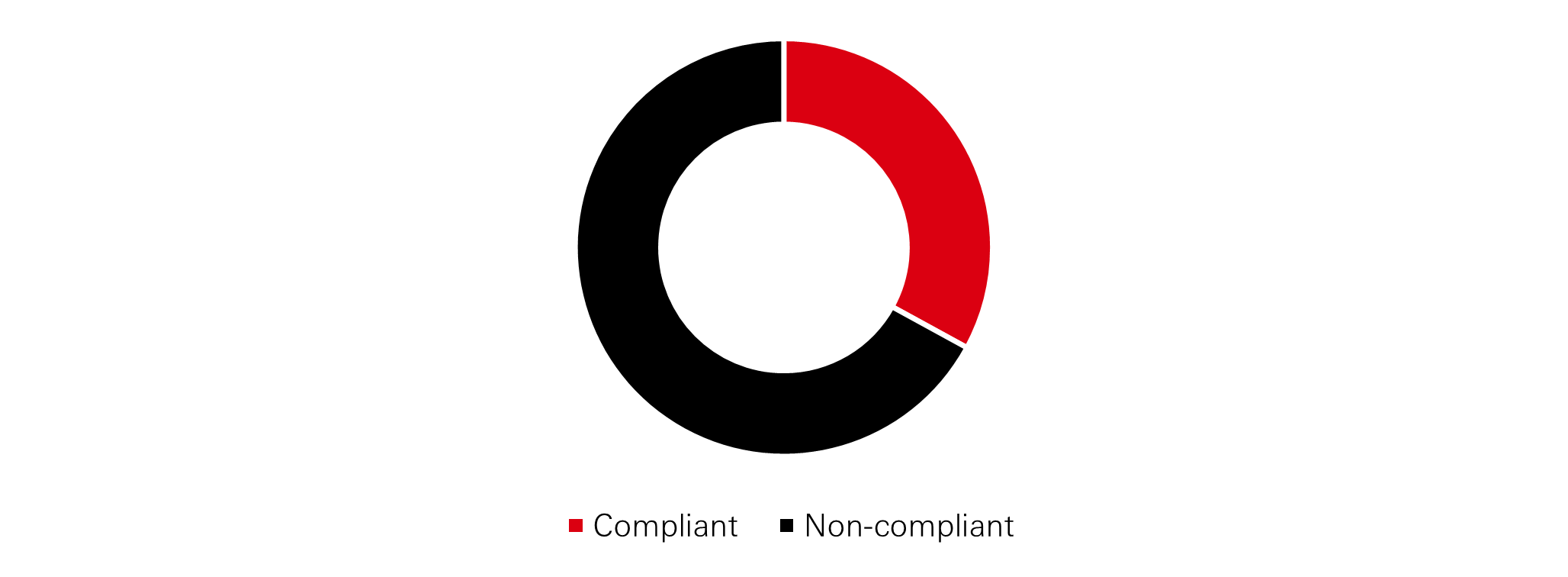

Applying the Shariah-compliant screens to the Core Infrastructure universe reduces its size by two thirds, i.e. from c. 380 to c. 120, across utilities, transportation, energy infrastructure and communications.

Exhibit 1: Impact of Shariah compliant screens (Compliant vs non-compliant)

Click the image to enlarge

Source: HSBC Asset Management as of 31 March 2026

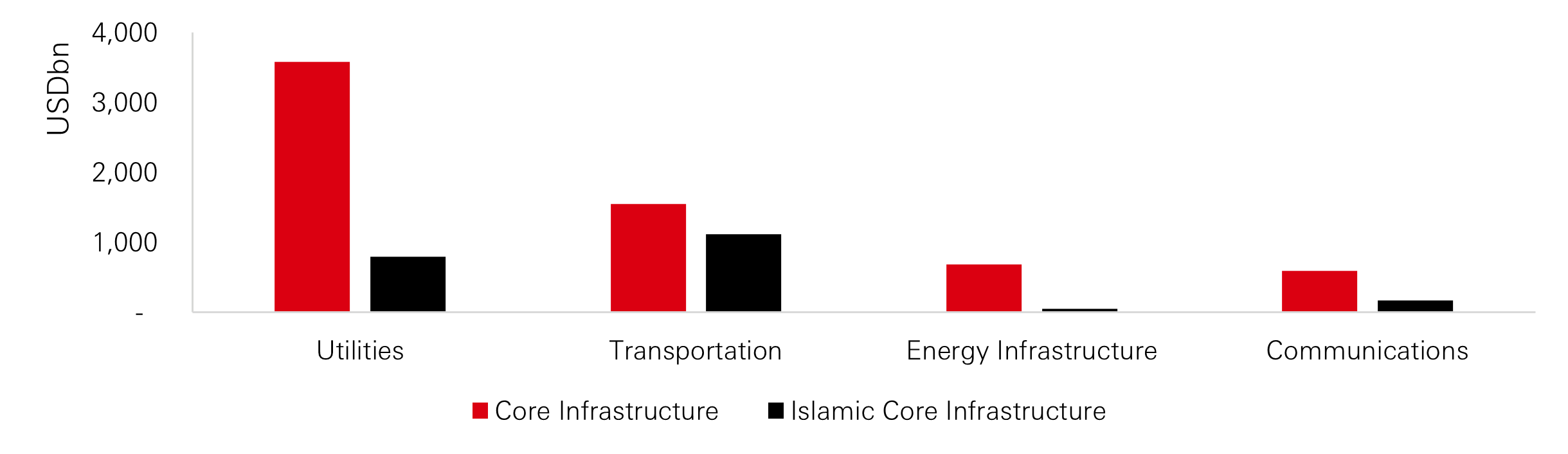

Exhibit 2: Market cap by sector (Core Infrastructure vs Islamic Core Infrastructure)

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

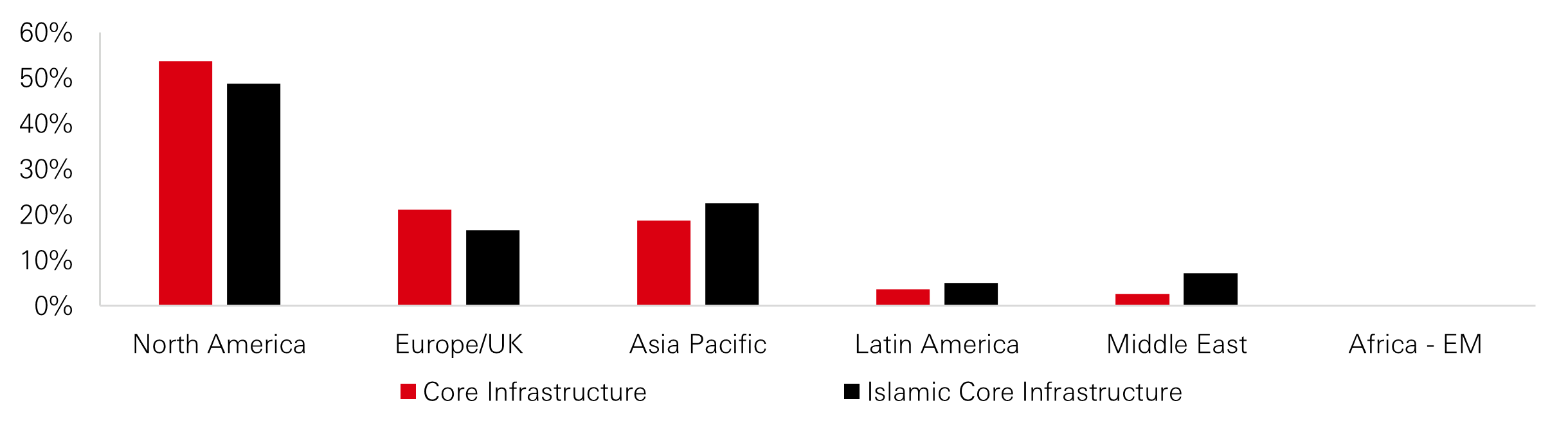

More importantly, for investors, Shariah compliant screening does not only reduce the number of eligible companies—it changes the shape of the opportunity set, shifting sector and regional composition. That reshaping matters because infrastructure sectors and regions have different sensitivities to macro drivers such as GDP growth, inflation and interest rates.

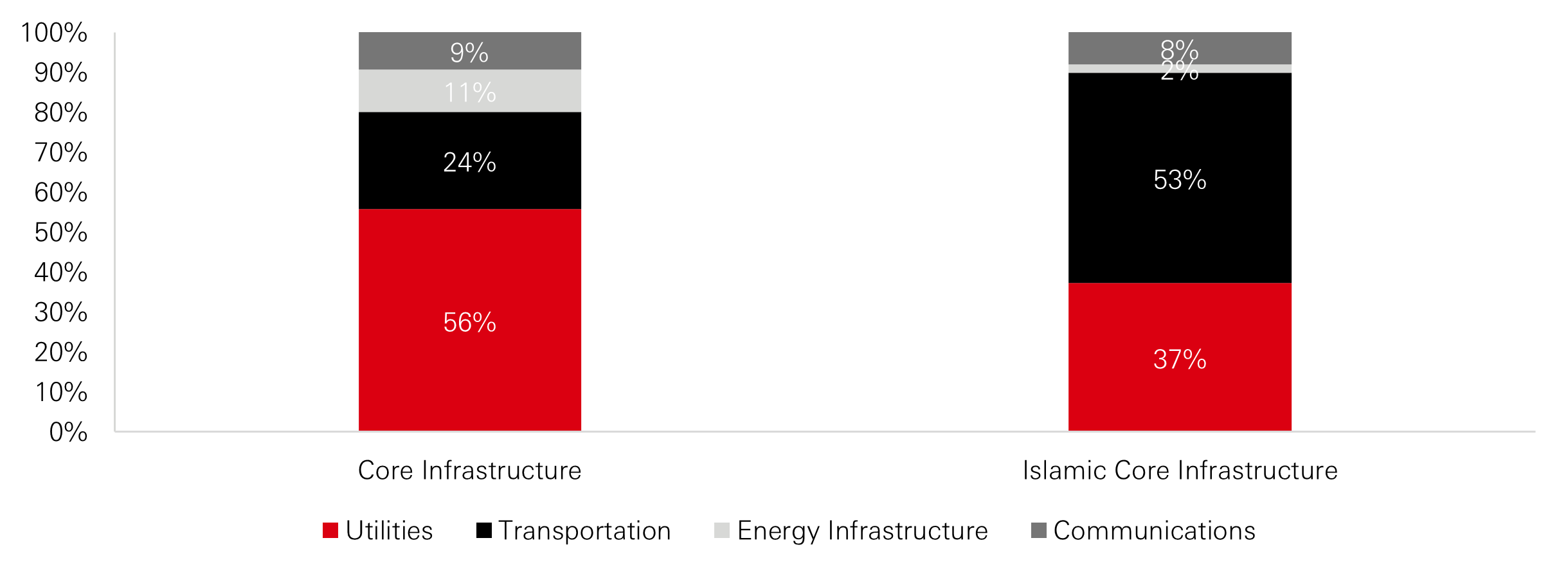

Exhibit 3: Sector mix shift (market cap weights)

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

Exhibit 4: Regional mix shift (market cap weights)

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

Macro sensitivities: Islamic infrastructure behaves differently

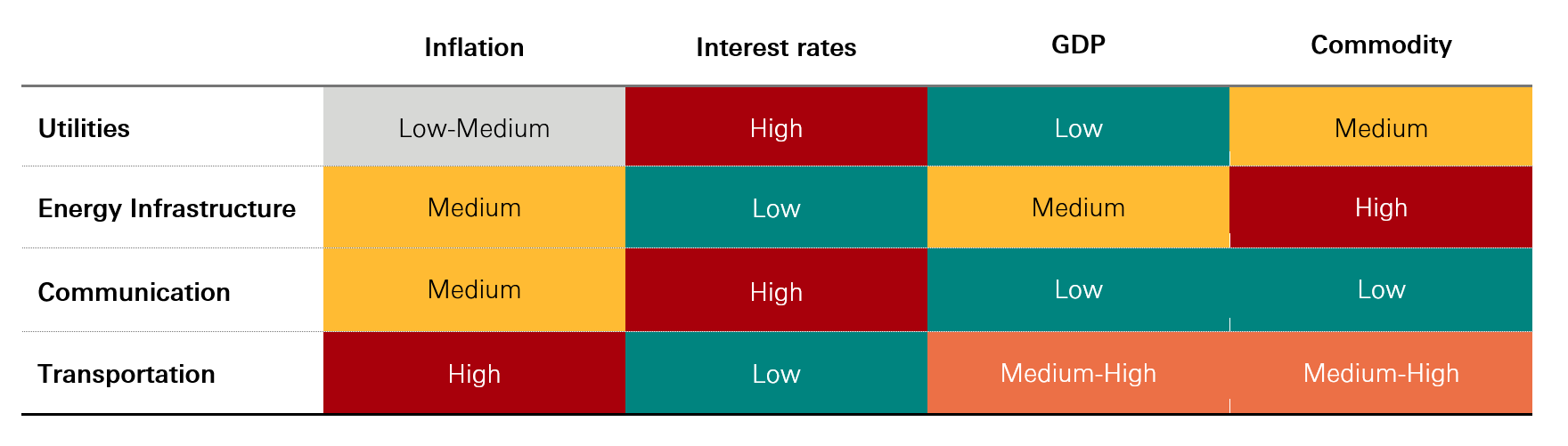

Different infrastructure sectors respond differently to macro conditions:

Exhibit 5: Macro sensitivity across infrastructure sectors

Click the image to enlarge

Source: HSBC Asset Management as of 31 March 2026

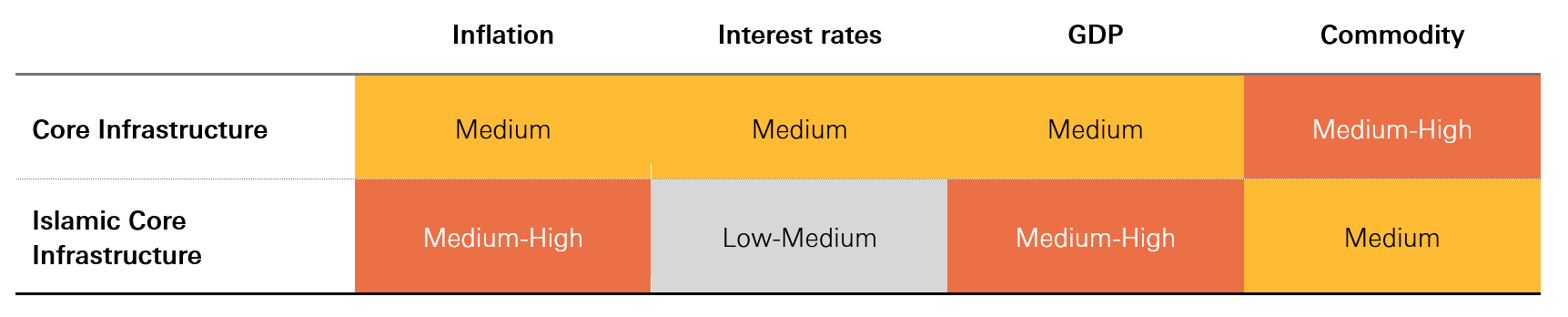

As shown in the table below, the different sector mix between the two universes can create a meaningful difference in overall macro sensitivities.

Exhibit 6: Macro sensitivity comparison (Core Infrastructure vs Islamic Core Infrastructure)

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

For investors, this is the key takeaway: Islamic infrastructure equities is not just “conventional infrastructure with exclusions”—it can deliver a different macro profile.

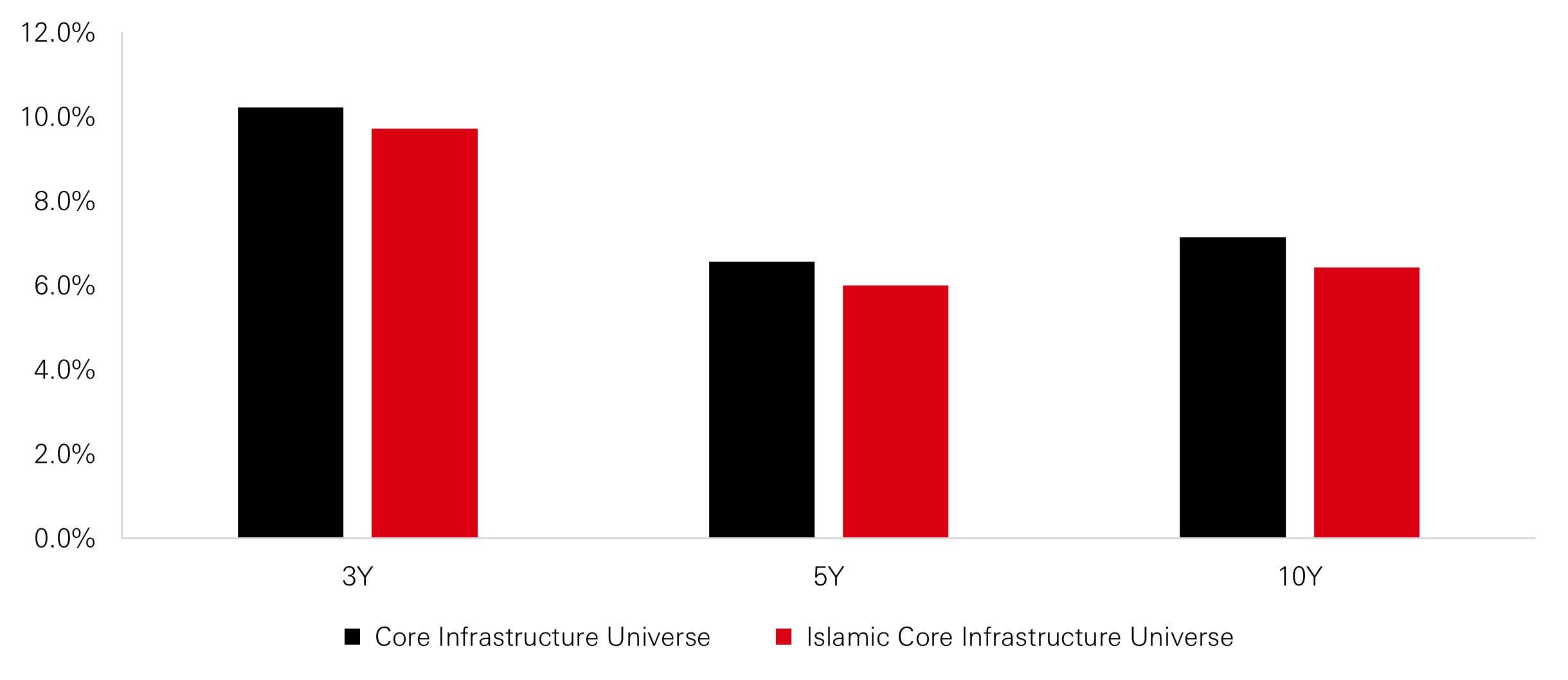

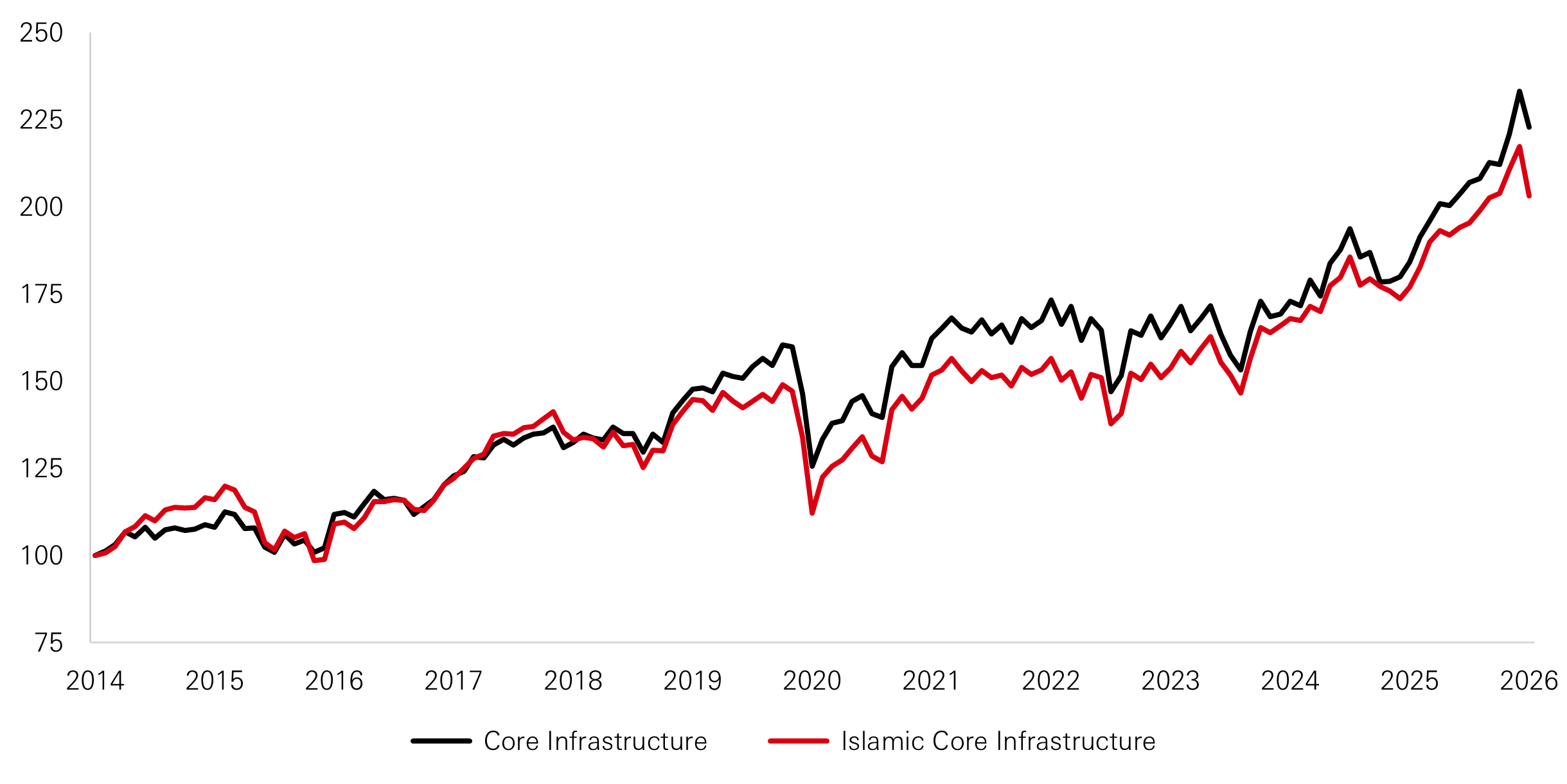

Despite the Shariah compliance screens changing the shape of the opportunity set, the historical performance between Core Infrastructure and Islamic Core Infrastructure is comparable in the medium to long term. It is encouraging to see that investors are not sacrificing return for compliance.

Exhibit 7: Medium-long term performance comparison

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

Exhibit 8: 10-year cumulative return comparison

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 March 2026

Filling a gap in Islamic equities portfolios

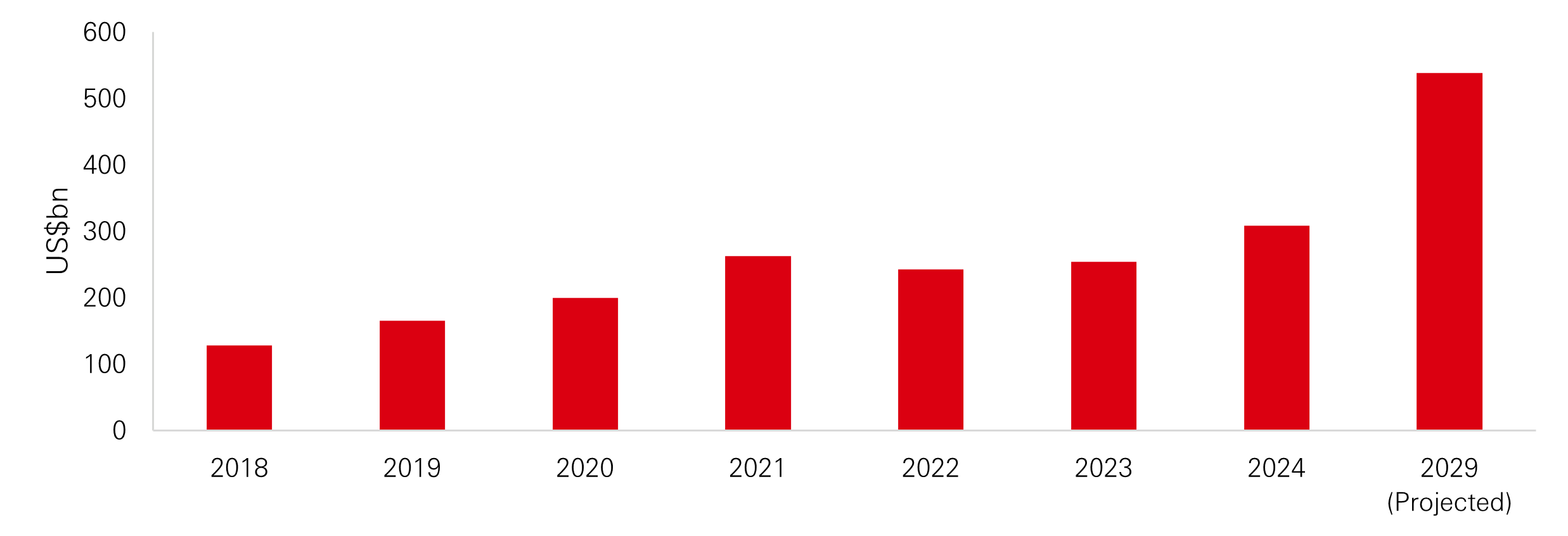

Islamic funds emerged in the 1980s and expanded rapidly in the early 2000s—first across Muslim-majority countries, and later in non-Muslim-majority markets such as the UK1. The Islamic funds market has continued to mature, with total Islamic funds AUM reaching USD308 billon in 2024 across 2,610 funds, and projected to rise to around USD538 billion by 20292.

Exhibit 9: Islamic funds AUM growth

Click the image to enlarge

Source: ICD–LSEG Islamic Finance Development Report 2025

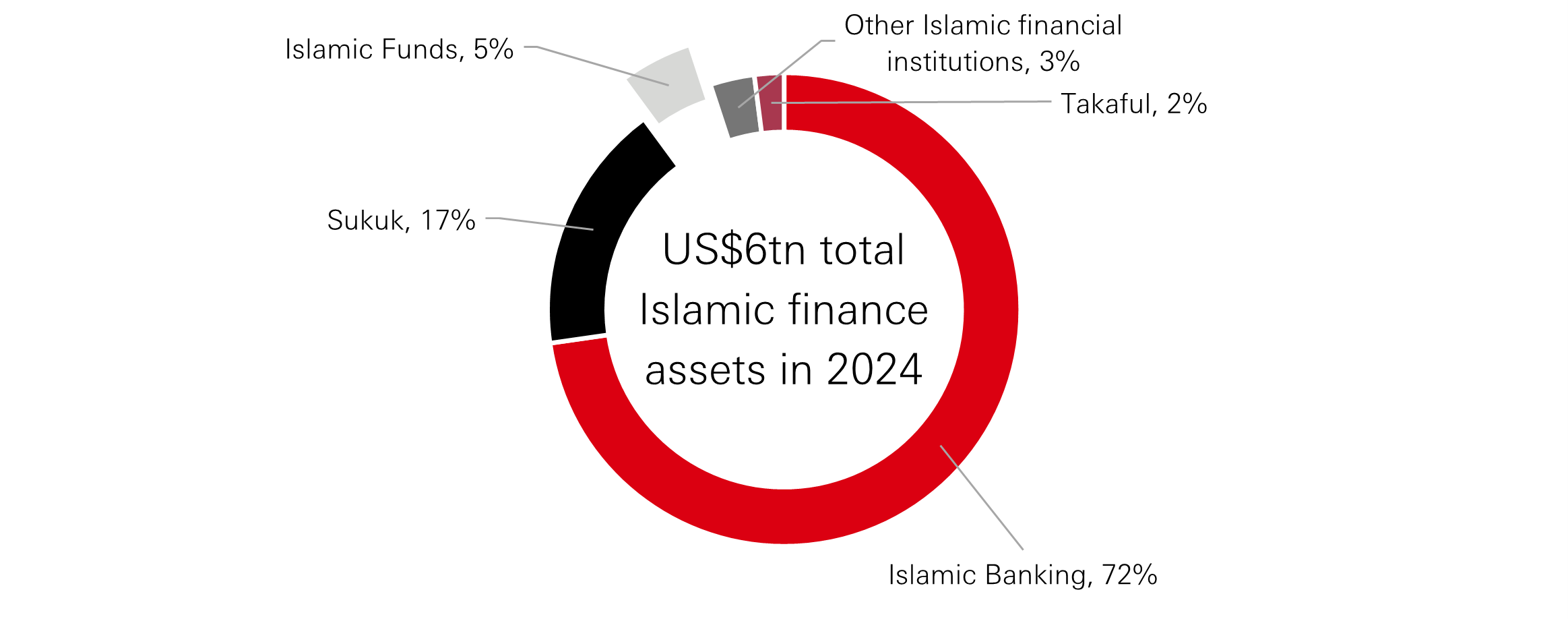

However, Islamic funds still represent a relatively small share of the broader Islamic finance ecosystem, and demographic tailwinds in favour of Shariah-compliant investing have not been fully reflected in fund markets. Compared to the conventional market landscape, there is a limited range of Islamic funds, which present challenges for investors seeking to diversify beyond broad Shariah-compliant equity exposures.

Exhibit 10: Islamic finance industry breakdown

Click the image to enlarge

Source: ICD–LSEG Islamic Finance Development Report 2025

And this is particularly relevant at a moment in which investors globally have been wanting to “broadening out” from the large exposure of equities’ indexes to mega-cap technology stocks, because of concerns on valuations and concentration risk. Shariah-compliant equity benchmarks tend to have an even heavier exposure to the technology sector, which may increase concentration risk for Islamic equities’ investors.

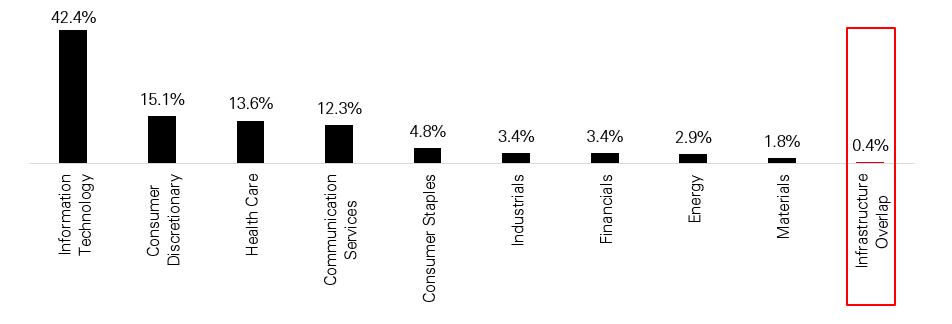

For example, the Dow Jones Islamic Market Titans 100 Index, a leading global equity benchmark tracking 100 of the largest Shariah-compliant companies, has over 40 per cent exposure to Information Technology, towering over all the other sectors including infrastructure (less than 1 per cent). Given the very limited exposure to infrastructure, a dedicated allocation to Islamic infrastructure equities offers the potential for diversification and can play a role as a more defensive component within an equity allocation — benefits that many investors may be seeking in a market environment where volatility is rising and inflation concerns are re-emerging.

Exhibit 11: DJ Islamic Market Titans 100 Sector Exposures

Click the image to enlarge

Source: Dow Jones as of 31 December 2025

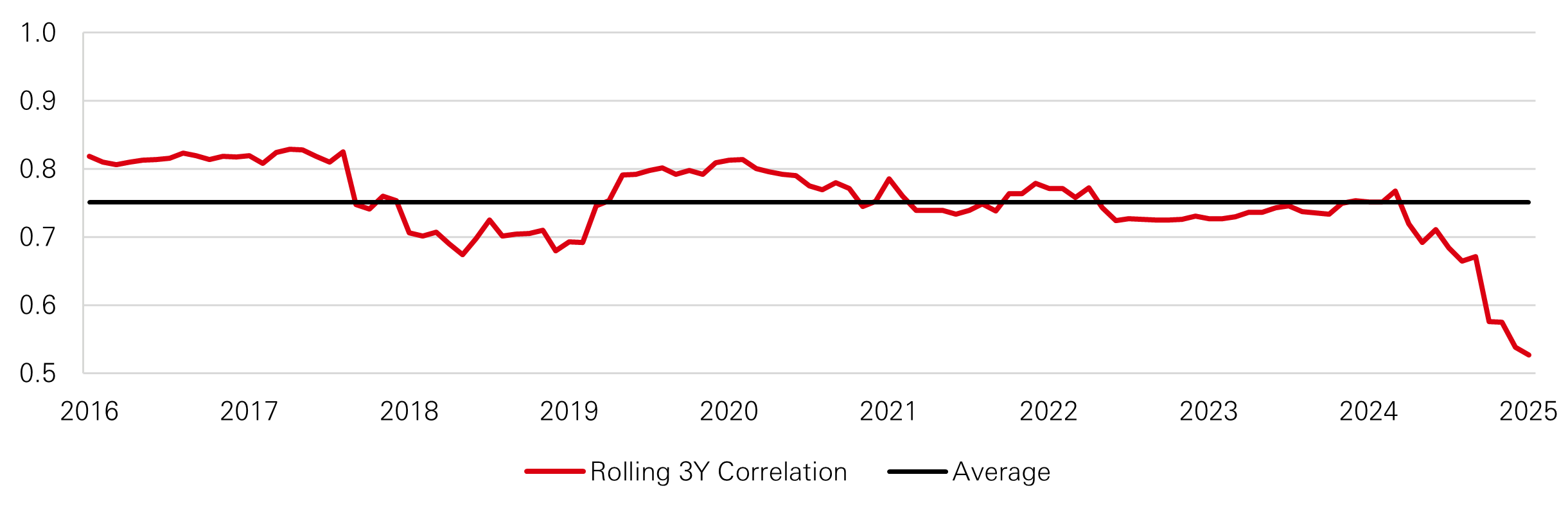

The potential for infrastructure to provide diversification benefits is also reflected in the correlation between the DJ Islamic Market Titans 100 and Islamic Core Infrastructure. As seen in Exhibit 12, historic correlation has averaged around 0.75 and has declined more recently. Ultimately, Islamic infrastructure equities can represent a very valuable building block for asset allocation consideration when managing an Islamic multi-asset portfolio.

Exhibit 12: DJ Islamic Market Titans 100 Correlation vs Islamic Core Infrastructure

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg as of 31 December 2025

Conclusion

Listed infrastructure equities can be an important defensive building block in diversified portfolios, offering exposure to essential-service assets with resilient and predictable cashflows, attractive risk-adjusted and de-correlated returns, and above-average income potential.

Shariah compliance reshapes the infrastructure opportunity set—reducing the eligible universe and changing sector and regional composition—but Islamic infrastructure equities remain a viable and compelling option for investors seeking infrastructure exposure within Shariah-based principles. For Islamic multi-asset portfolios in particular, they can help address diversification constraints and reduce concentration risk from tech-heavy Shariah equity benchmarks.

1TheCityUK (2022). Islamic finance: global trends and the UK market

2ICD–LSEG Islamic Finance Development Report 2025

Diversification does not protect against loss, nor does it guarantee profit.

Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

Key Risks

Further information on the potential risks can be found in the Key Investor Information Document (KID) and/or the Prospectus or Offering Memorandum.

There is no assurance that a portfolio will achieve its investment objective or will work under all market conditions. The value of investments may go down as well as up and you may not get back the amount originally invested. Portfolios may be subject to certain additional risks, which should be considered carefully along with their investment objectives and fees.

- Equity Risk: Portfolios that invest in securities listed on a stock exchange or market could be affected by general changes in the stock market. The value of investments can go down as well as up due to equity markets movements.

- Interest Rate Risk: As interest rates rise debt securities will fall in value. The value of debt is inversely proportional to interest rate movements.

- Counterparty Risk: The possibility that the counterparty to a transaction may be unwilling or unable to meet its obligations.

- Derivatives Risk: Derivatives can behave unexpectedly. The pricing and volatility of many derivatives may diverge from strictly reflecting the pricing or volatility of their underlying reference(s), instrument or asset.

- Emerging Markets Risk: Emerging markets are less established, and often more volatile, than developed markets and involve higher risks, particularly market, liquidity and currency risks.

- Exchange Rate Risk: Changes in currency exchange rates could reduce or increase investment gains or investment losses, in some cases significantly.

- Investment Leverage Risk: Investment Leverage occurs when the economic exposure is greater than the amount invested, such as when derivatives are used. A Fund that employs leverage may experience greater gains and/or losses due to the amplification effect from a movement in the price of the reference source.

- Liquidity Risk: Liquidity Risk is the risk that a Fund may encounter difficulties meeting its obligations in respect of financial liabilities that are settled by delivering cash or other financial assets, thereby compromising existing or remaining investors.

- Operational Risk: Operational risks may subject the Fund to errors affecting transactions, valuation, accounting, and financial reporting, among other things.

- Style Risk: Different investment styles typically go in and out of favour depending on market conditions and investor sentiment.

- Model Risk: Model risk occurs when a financial model used in the portfolio management or valuation processes does not perform the tasks or capture the risks it was designed to. It is considered a subset of operational risk, as model risk mostly affects the portfolio that uses the model.

- Alternatives: There are additional risks associated with specific alternative investments within the portfolios; these investments may be less readily realisable than others and it may therefore be difficult to sell in a timely manner at a reasonable price or to obtain reliable information about their value; there may also be greater potential for significant price movements

For Professional Investors only and should not be distributed to or relied upon by Retail Clients.

Important Information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian branch of HSBC Global Asset Management (France), regulated by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy;

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agency;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D070041_v1.0 ; Expiry Date: 30.04.2027